Flower Pricing for the Canadian Cannabis Market

Flower Pricing for the Canadian Cannabis Market

Flower is, should, and will always be the category with the highest SKU concentration in the cannabis industry. But with all this competition, how much should an LP charge at retail for their flower?

Well, they should target a retail price of about $0.45/gram per percentage of THC contained in the product.

Alright, alright, alright. How can anyone make such a general statement like that and stand by it? Read on to find out why $0.45 was chosen.

Flower is Still King

Working in this industry, one can quickly shift their focus to only focusing on more novel products such as edibles, concentrates and vapes. There have been many changes with cannabis products and an evolution over the years. Pre-dating legalization, the boundaries of what cannabis products are, have been challenged. Derivative products such as vapes, diamonds, shatter, topical creams, bath products, tinctures, edibles and many more, have been pushed to the forefront of the industry. Trotted out as the next wave of cannabis during cannabis 2.0 legalization.

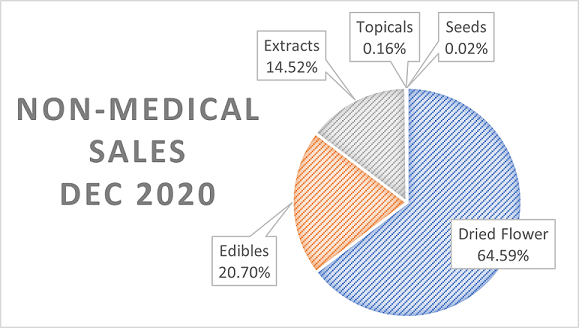

But, it has been over a year and a half since 2.0 legalization and flower still reigns supreme. Looking at the December 2020 sales results from Health Canada, flower accounted for nearly 65% of all non-medical cannabis sales. Plant sales have been omitted as they have even less sales volume than seeds.

Data source: Health Canada

The flower category faces the fiercest competition of all. As of writing, there are 700 SKUs listed in Alberta and 315 in BC in the flower/pre-roll categories. What’s the second most competitive category? Vape, which has “only” 221 and 104 SKUs listed, respectively. To take a closer look at other where the market started just at the beginning of the year with respect to SKU counts, check out our other article titled “Growth Predictions for the Canadian Cannabis Industry in 2021” here.

THC, Terpenes, or what? The current state of affairs in cannabis

There are a lot of factors that make cannabis what it is. THC, terpenes, moisture, colour and the entourage effect all play a part in the experience, and it doesn’t stop there. The more one immerses into the industry, the more difficult it is to remember that most consumers do not share the same level of education or foundational knowledge yet to have a proper grasp of the impact of these terms.

Remember that the regulated Canadian cannabis market is still in its infancy. It does not yet emulate the sophistication of the beverage alcohol industry in terms of consumer preference. When going in to buy a beer, wine or spirit, it is rare that one looks at the alcohol percentage to see how strong it is. We are preconditioned with baselines already. Beer comes in around 5%, wine 13%, and spirits 40% The cannabis market does not share this trait.

A recent report released by Deloitte surveyed existing consumers to rank attributes that they associate with quality cannabis. Among the items are quality of “high”, taste, smell, duration of “high”, bud density, moisture content, terpene mix, and THC and/or CBD content. THC and/or CBD content ranked at the top of the chart. Simply, how potent your flower is matters to the consumer.

There has been much discussion around THC and flower. LPs trotting out their highly potent, quad-grade flower, immensely proud of their achievements of cranking up potency to new extremes. Hitting upwards of 30% (300mg/g) THC.

On the other hand, we have LPs voicing their displeasure around the focus on THC and CBD in flower. Many are pushing for increased transparency for other factors with the most prominent of these being terpene content. Terpene percentages are now being released by LPs more regularly to hopefully add an additional speaking point beyond simply THC percentage and increase transparency.

Reading reviews of flower online, it is a mixed bag. Some products with 17% (170mg/g) flower has reviews of feeling very potent while 24% (240mg/g) flower comes up short. Then, flower with 6% terpene content apparently doesn’t taste as good as a batch with 3.5% terpene content.

With all of this mixed information and the number of new consumers in the industry, it is no doubt that consumers gravitate to putting weight on the one concrete number presented on the package. Potency.

With all this back and forth between what quality flower means, it is important to examine how LPs are pricing to look for motivations. Is it THC/CBD content, terpenes, or perhaps something else that drives the price?

How LPs price their flower

Despite the above back and forth, it appears to be heavily connected to THC potency. Of course, this is stated with data to back it up.

About the Data

Due to simplicity and ease of information access, the data looks at Alberta and British Columbia government-run online marketplaces as of April 1st, 2021. The data only contains 3.5g package formats as this is the product size that has the highest SKU density. Others are not included in an effort to reduce variables which would skew results. Typically, an LP will charge more per gram in smaller formats (ie 1g) and less per gram in larger, value-sized formats (ie 7g, 14g, and 28g).

Due to labeling regulations, products are given a high and low THC/CBD potency range to fall within. The average was taken off the ranges provided. Further, gaps in the graph are due to there not being any products that fall within that THC level.

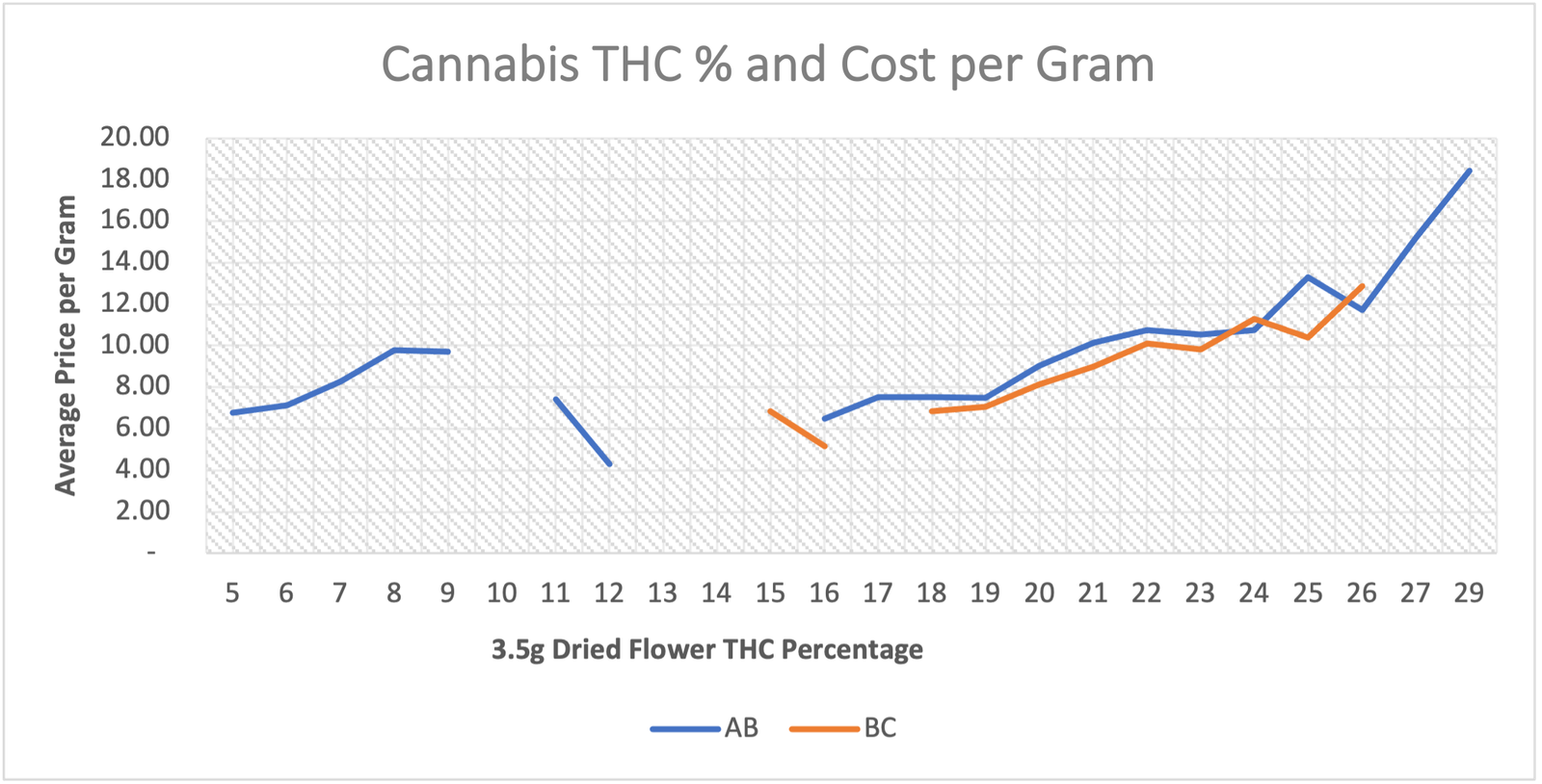

Cannabis THC Percentages and Cost per Gram

Data source: albertacannabis.org, bccannabisstore.ca on April 1, 2021

The chart above compares costs per gram of flower in each THC potency percentage. The left side of the chart, which shows THC potency ranges in the 12 or less range, is due to these being more CBD-forward products. These products exist for a different reason than THC dominant strains and are shown to display the whole market range of products that do exist. CBD is cool too! Also, it reveals something: LPs are charging prices equal to 18-20% THC flower for their CBD- forward flower.

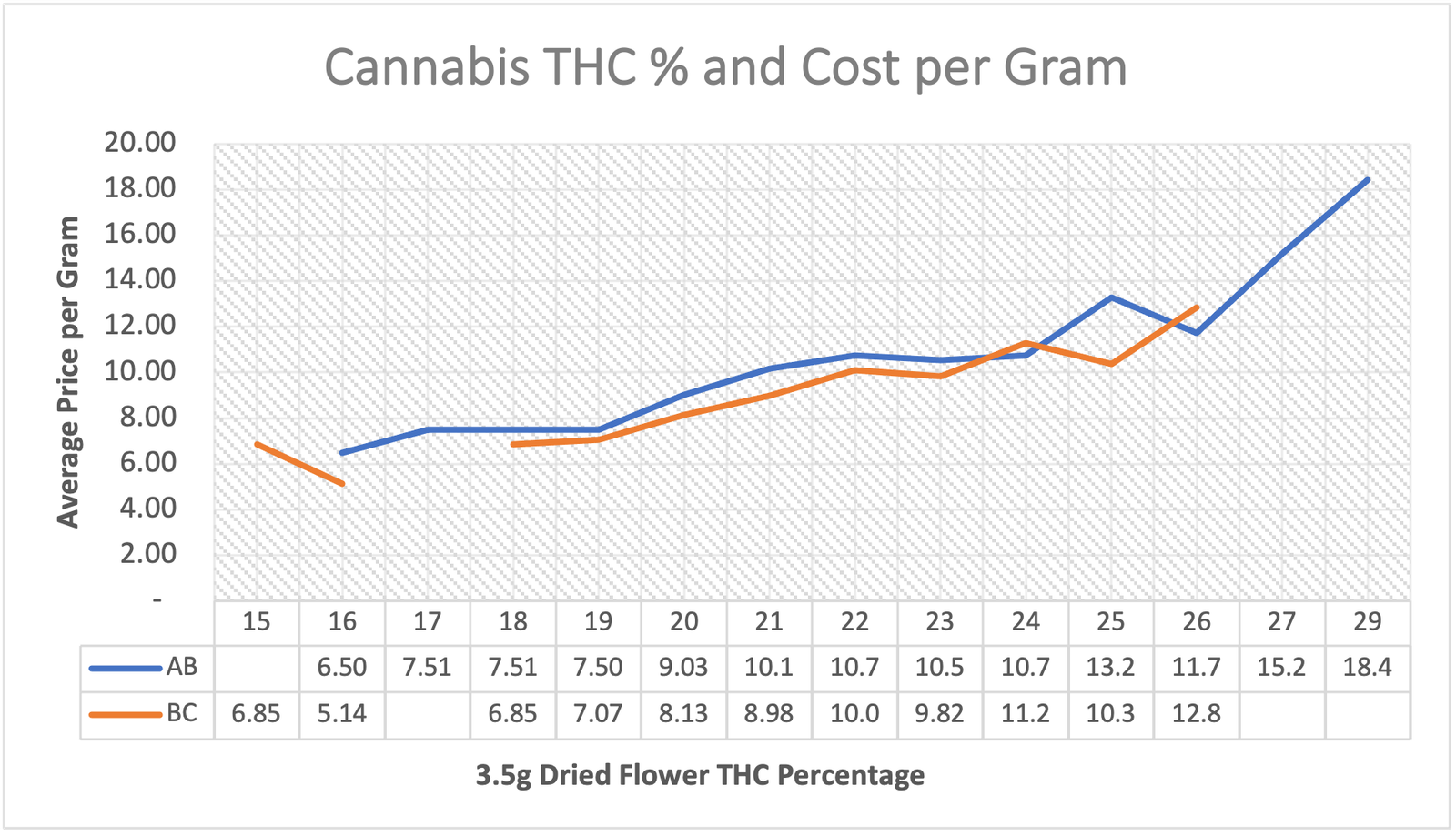

Data source: albertacannabis.org, bccannabisstore.ca on April 1, 2021

The above chart crops off the CBD heavier flower. It shows that there is a steady increase in the retail price per gram at retail as the THC percentage increases. Going in, this was expected but it presents clear evidence that this is the case. Once the THC percentage average hits around 27%, there is a shift upwards, looking like there is a true premium being charged for these high THC SKUs.

This begged the next question. Are LPs charging more for 24% THC flower than 18% THC flower just because of higher THC content?

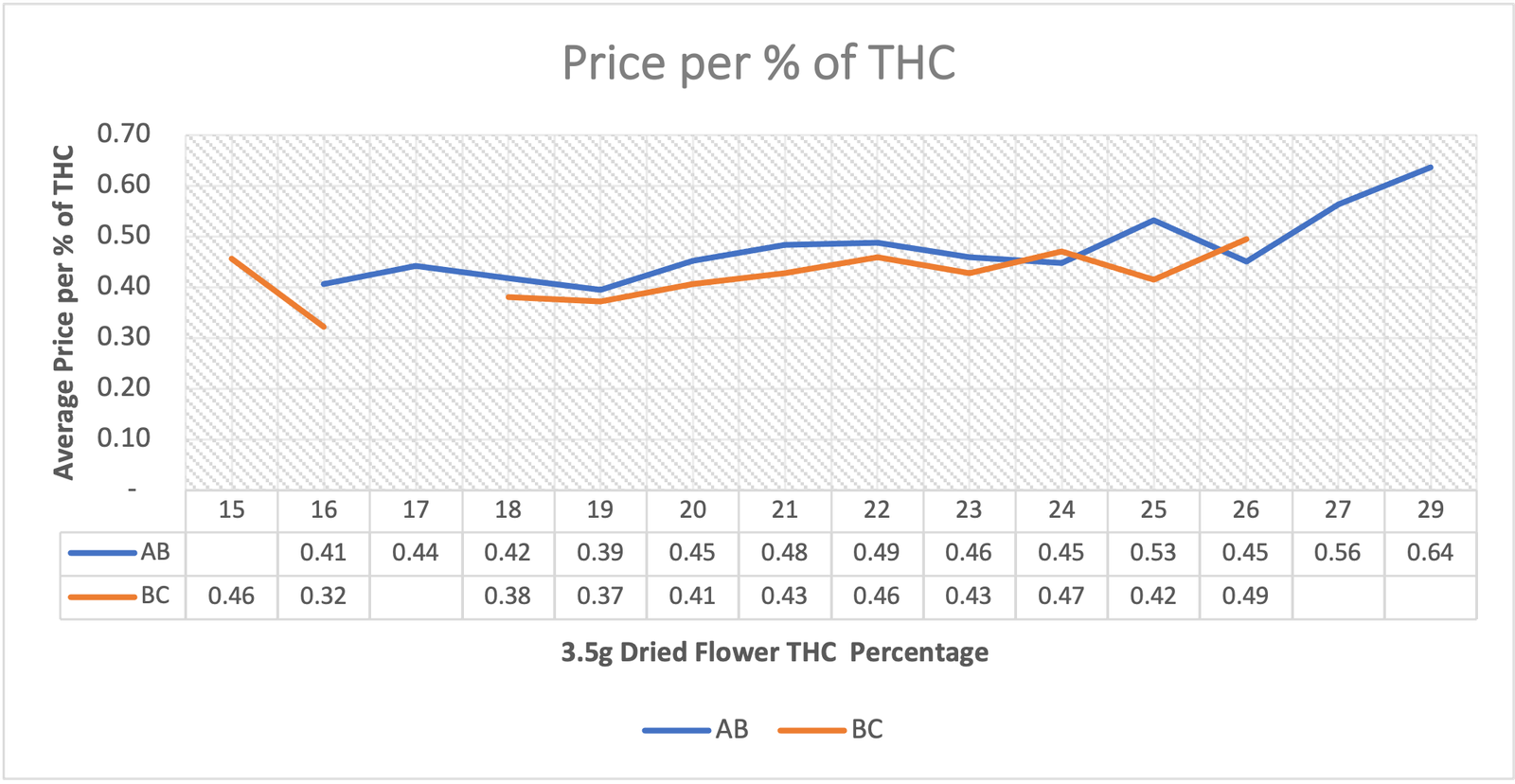

Average Price per Percentile of THC in 3.5g Flower

Data source: albertacannabis.org, bccannabisstore.ca on April 1, 2021

Short answer: it sure looks like it. Between the 15% through 24% THC range, the line is quite flat. It does increase gradually showing a small premium for each additional percentage of potency in flower but not a heck of a lot.

The data points below the chart show that the $0.45 per one percent of THC in the product mentioned earlier, is close for flower in the 18-24% THC classifications. Using the $0.45 per percentage, we expect that a 18% SKU would list for $28.35 while a 24% SKU would list for $37.80.

Because:

- 18 THC “points” x $0.45 per percentage x 3.5 grams = $28.35 (or $8.10/g)

- 24 THC “points” x $0.45 per percentage x 3.5 grams = $37.80 (or $10.80/g)

Taking it back to alcohol as an example, if a spirt was 20% alc./vol and cost $20.00, then a 40% alc./vol would cost $40.00. The extra amount is just due to increased concentration of alcohol.

Check the marketplace and of course this is a generalization. Working with averages means extremes will be found on either end of the ranges. However, the data above reveals that there seems to be a correlation between cannabis flower price and potency with only small premiums being charged for each additional percent increase in potency. It isn’t until the 25%+ THC range that a more significant premium is being paid for that higher THC potency.

If additional factors were being priced into the market beyond THC potency, such as terpene content, this line would not be so smooth. More variation would be included in the middle sections, that would skew the chart one way or the other.

Possible Motivations for LPs to Chase High Potency

- Clout. It can’t be denied that being able to grow high-quality cannabis will earn the growers and company points with consumers and industry peers. As THC content is the most recognized attribute of quality by the average consumer, the LP will gain brand share.

- Quick sales. Highly potent weed sells. Quickly. If time is spent looking at online stores, it doesn’t take long to see that highly potent lots/strains do not stay available long. Further, quick sales mean they are decreasing their risk of old, stale inventory sitting around.

- More dollars per sq/ft of grow space. Not all LPs are huge behemoths with vast greenhouses. Every increase in percentage means that they can profit more out from their limited grow and storage space. With space limitations, delivering on potency is a way to increase revenue.

- There is a THC premium. It may not be steep but there is a premium being paid by the consumer for higher levels of potency in their flower and it gets steeper the more potent it is.

- Taxes. Unlike with concentrates where excise taxes are tied to mg of THC in a product, flower is taxed by weight. There is nothing to discourage LPs from trying to get the highest percentage they can.

- Decrease in competition in the higher ends. Last on this list, but certainly not least, growing high THC flower puts the product into a new class, above competing products. Here are the SKU concentrations listed in each THC potency category for the Alberta and British Columbia markets.

As can be seen, if an LP grows flower that yields a potency of 20% to even 24%, there is a lot of competition. Only very few are coming in at a listed 25%+ potency. Right now, being listed there would make it easier to differentiate.

The Takeaway

THC is far from the only aspect to flower. The plant has so much to offer beyond just this one property. LPs are taking different positions in their pricing and have a wide variety of qualities of flower available. Some are premium pricing what they think is their best stuff, while others are line pricing all their products. Every LP is going to have their own approach, based on the market they are targeting.

However, it is important to look at where the market is. Resources are going to be dumped into the build, grow and packaging of product and not having a proper handle on what is currently motivating consumer purchases will cripple the investment as no market share will be gained.

Further, poorly priced items will slow sales, bring on delisting’s and potentially the dreaded product return. With thinning capital in this industry, sell-through equals success. Failure to achieve this sell-through, for whatever reason, will bring any goliath to their knees eventually.