Growth predictions for the Canadian cannabis industry in 2021

Well, this presumptive confidence highlighted in the hilarious sitcom Brooklyn Nine-Nine was definitely the view of cannabis prior to legalization. Prior to there being 598 (as of writing) licensed producers in Canada competing for their segment of the cannabis market and before the veritable labyrinth of Health Canada regulations made bringing brands to life a fight-for- your-life struggle. It might not be where everyone might have hoped it would be at this point – more like the bigger, better and badder illicit market – but it sure has come along way since legalization in October 2018.

Despite the tumultuous year that was 2020, it wasn’t all bad. Yes, there were plenty of insolvencies, sell-offs and market shifts, plus an international pandemic to contend with, but overall, it was big for the Canadian cannabis market. The launch of cannabis 2.0 products, which only really began in January 2020, finally gained some velocity in a few market segments and started to push this market to new heights.

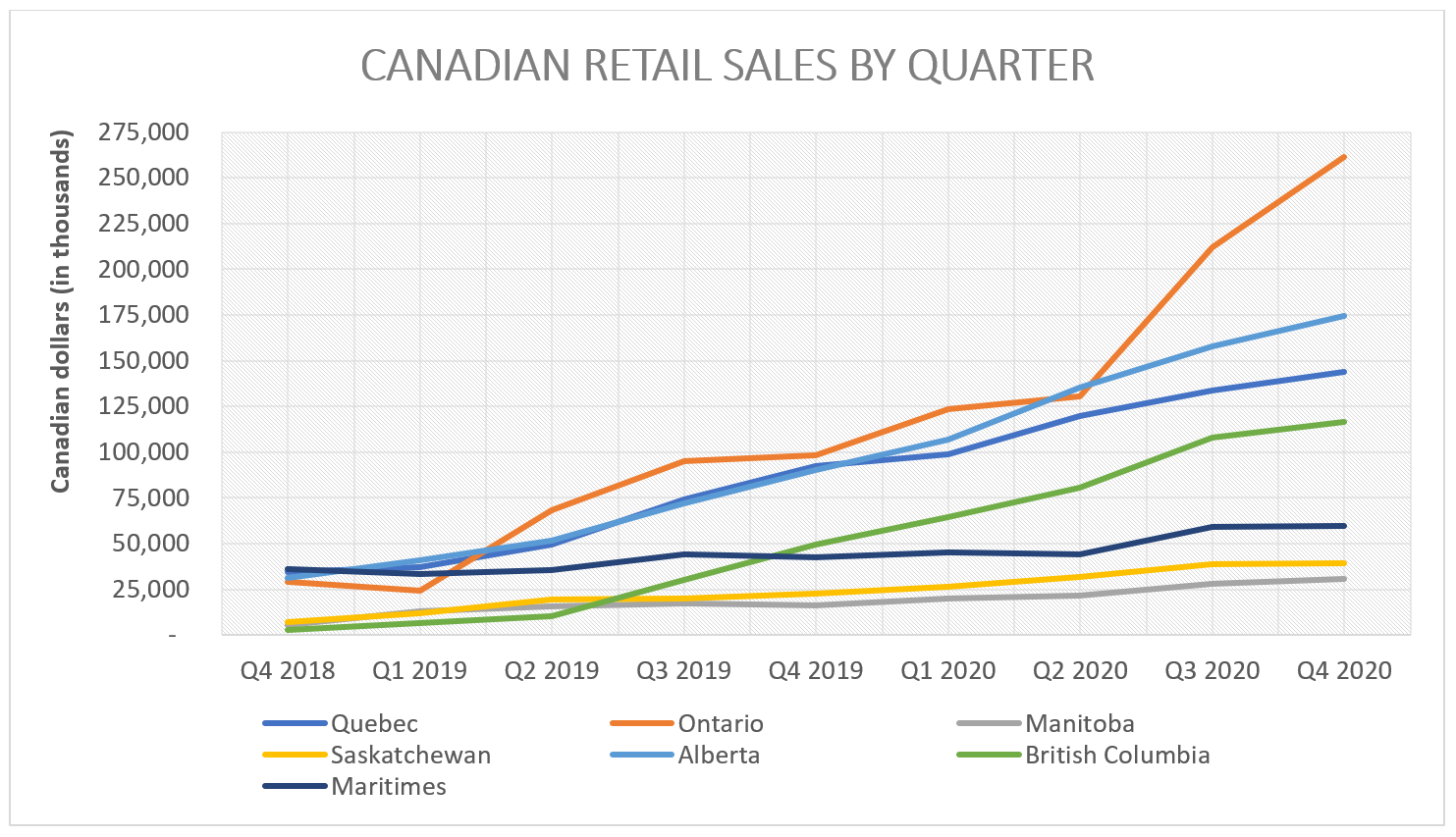

Taking a look at the most recent available market data from Health Canada, gross revenue of retail cannabis sales has grown to $260-270 million CAD per month. Annualizing this, the annualized retail market size is sitting around $3.2 billion. Not bad.

Data source: Health Canada

Predictions for the 2021 Canadian Cannabis Market

Now it is time to speculate. Given the relatively consistent monthly upswing in sales driven by increased retail market locations, consumer adoption and product diversity, making some predictions about where it will be come December 2021 is a good idea. Using this information, setting expectations and projections around what it will mean when a certain percentage of market share is captured. How much revenue is that going to mean for the company? If one can retain market share percentage, where will sales revenue end up with the overall market size increasing? Can operations keep up with these expected demands?

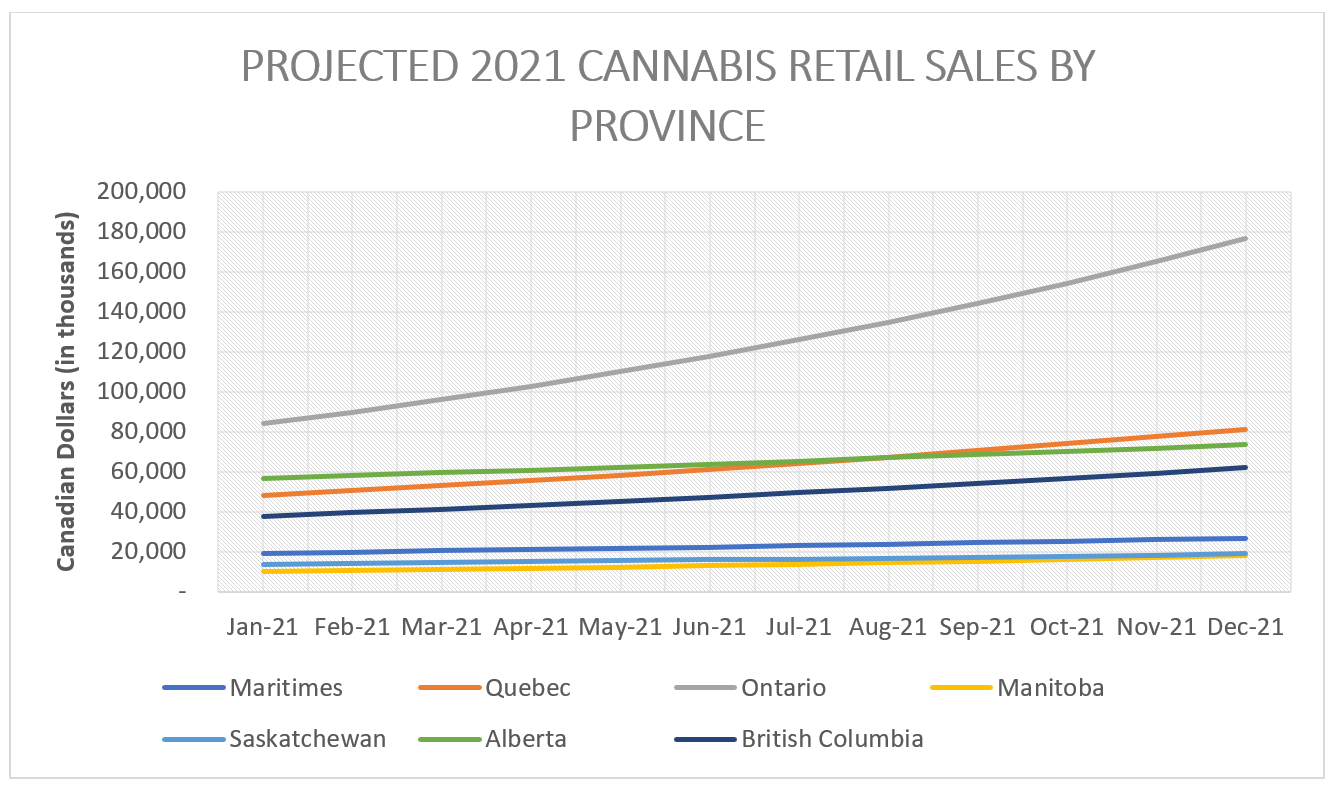

Based on the growth over the past calendar year and overlaying some similar expectations to this one, expected cannabis retail sales will be $4.2 billion while the month of December will end with revenue over $450 million. Annualizing December projected revenue, the annualized cannabis retail sales market will be $5.4 billion. This is with the expectation that monthly per capita spending is going to increase to $9.00-16.50 across markets that have yet to achieve that mark. Ones already there will also continue to increase but less drastically.

Looking at figures from the alcohol industry in Canada and examining the national per capita spend annually in 2017 per statista.com was $1,098; or $91.50 monthly. Comparing some of the largest markets in Canada such as Ontario and Alberta at $5.69 and $12.78, respectively, if there were concerns of cannabis taking over significant market-share from alcohol, there is a way to go yet.

The above chart uses an average expected month over month growth percentage, ignoring seasonal adjustments. The large swing in Ontario is a result of their per capita spending being expected to increase to just shy of $12.00 per month by the end of this calendar year. That’s right. It’s going to DOUBLE in 2021. Given the influx of retail stores coming online, it should be expected that Ontario can achieve Alberta’s per capita figures of this year. The Ontario market has so much more to give.

Factors Driving Market Growth in 2021

There are several factors that are going to contribute to the success of the Canadian cannabis retail market this year.

- Increased consumer awareness due to more effective branding and advertising strategies.

- Decreasing stigma associated with cannabis use as awareness and knowledge is shared amongst the populous.

- Increase in cannabis retail locations.

- Increase in diversity and competition of product offerings.

- Continued shift away from the unregulated market driven through value, ensuring safe supply and a vast selection.

Competition of Brands in the Market Entering 2021

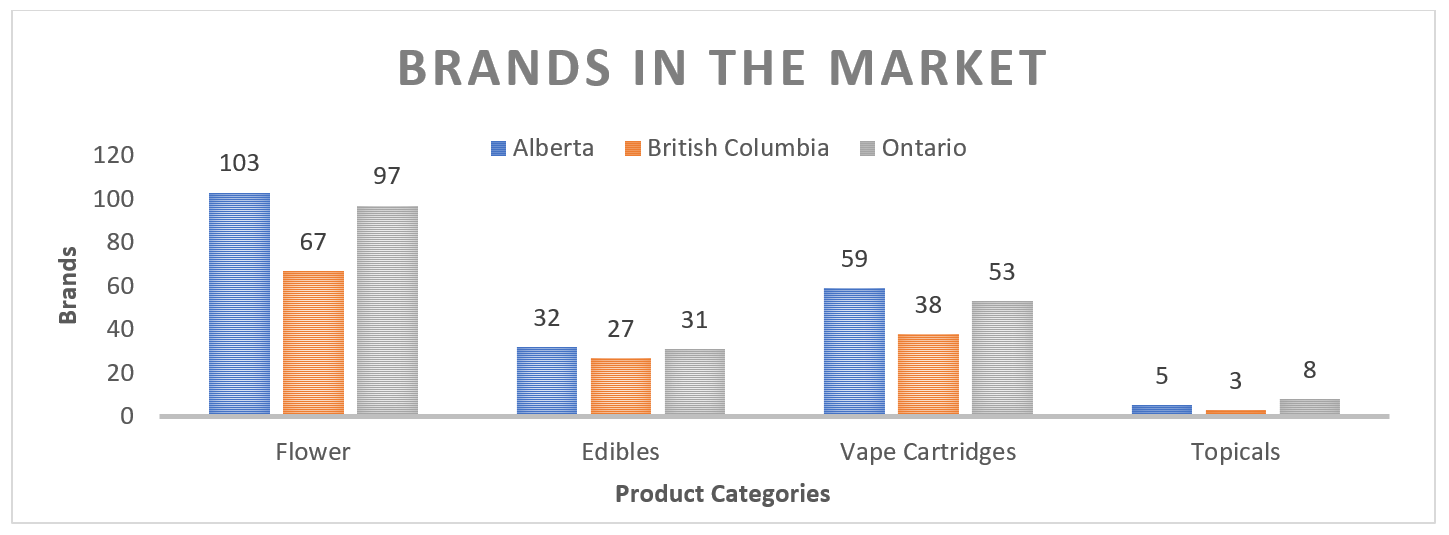

Data sources: bccannabisstore.ca, ocs.ca, albertacannabis.org on Jan 1, 2021.

The Fight for Flower is Fierce

Naturally, the most competitive market is the flower product category. That shouldn’t come as a surprise as with just a glance at the LP listing on Health Canada and shows the percentage of LPs authorized to sell and distribute dried flower in comparison to those with licenses authorized to sell and distribute extracts, edibles and topicals. Further, dried flower is typically the first product to market for most LPs, which is going to result in it being the stiffest category for competition. As seen above, there are 103, 67, and 97 brands in the market in Alberta, British Columbia, and Ontario respectively, as of January 1, 2021. The category with the second most participation is for vape cartridges, thirdly, comes the edibles market and last, the under appreciated topicals space. Not mentioned is the other concentrates category outside of vape. This sector is starting to see some action, but it just isn’t there yet. It is great to see shatters, kief and hash of all iterations, finally reaching the regulated space but there aren’t many options…yet.

Why it matters

Examining the industry overall to see the brand concentration is an important first step in examining where new entrants will be more likely to stand out from the crowd or get lost in the shuffle. Edibles continues to remain a top category with plenty of white space for a more diverse product set to be introduced. Further, the almost barren wasteland that is the topicals space, continues to present itself as rich an opportunity as any seen before.

2021 BRAND PREDICTION

This is subject to many variables. One of which is the preference of distributors looking to bring in new brands which could be new LPs versus favouring their existing relationships with LPs looking to extend their existing brands. Category saturation is also quickly becoming a main point for consideration. Where is the ceiling when it comes to each category? This is a bit of a dice roll given that it is up to the mercy of the distributors looking to carry more stock but this industry is for the brave.

| PREDICTION OF BRANDS IN THE MARKET AS OF DECEMBER 2021 | ||||||||

| Flower | Edibles | Vape | Topicals | |||||

| JAN 1 | DEC 31 | JAN 1 | DEC 31 | JAN 1 | DEC 31 | JAN 1 | DEC 31 | |

| British Columbia | 67 | 110 | 27 | 90 | 38 | 80 | 3 | 15 |

| Alberta | 103 | 170 | 32 | 110 | 59 | 90 | 5 | 18 |

| Ontario | 97 | 180 | 31 | 120 | 53 | 95 | 8 | 21 |

New brands are coming. Into the third-year post legalization, maturing companies are steadily launching new products in targeting different market positions. There are still new LPs just coming online now but the process of getting to market is slowing down and becoming more structured, which is going to slow brand expansion. In 2021, edibles brands will overtake the vape category. Ontario will usurp Alberta as the most diverse province in terms of available brand offerings.

SKU Concentration of Cannabis Products

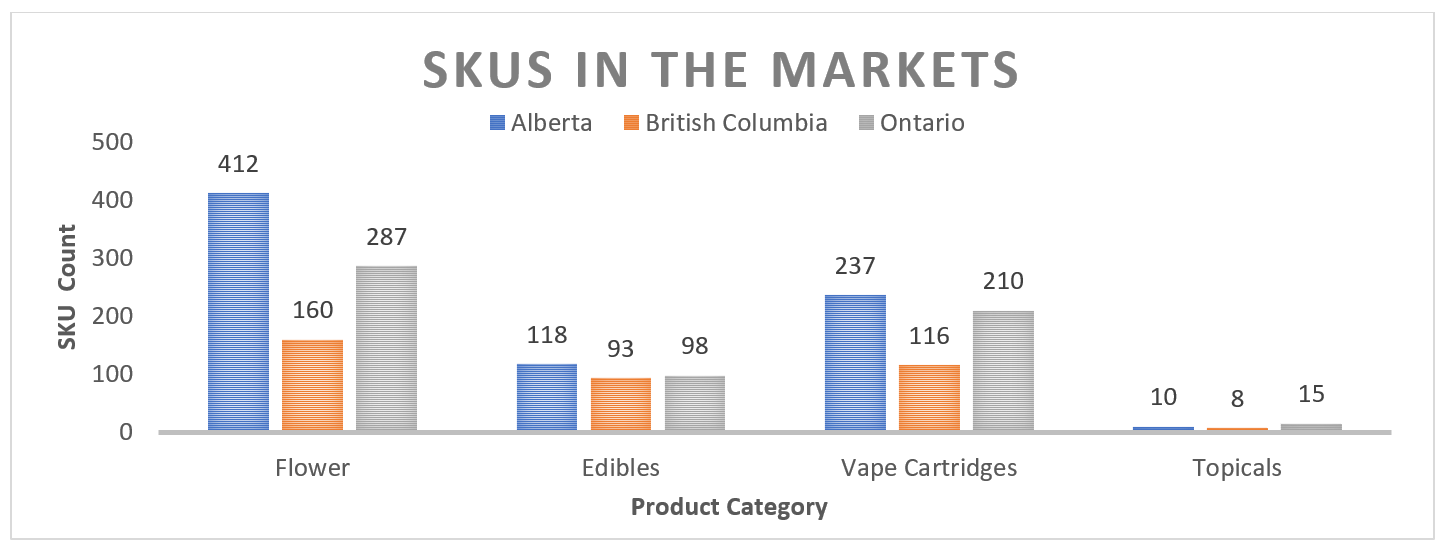

Data sources: bccannabisstore.ca, ocs.ca, albertacannabis.org on Jan 1, 2021.

Looking at the count of SKUs available in each category, it shows that those brands brought a whole lot of SKUs with them. For every brand present in the Alberta flower market, there is on average, four SKUs under each umbrella. Nearly each market’s brand-to-SKU ratio is between three to four with the exception of BC flower and topicals across the board demonstrating that there isn’t the same depth of brand penetration in those segments as with the other markets.

Similar to looking at the overall brand concentration, examining SKU count by category highlights where new-to-market SKUs will likely have the easiest time competing and gaining a spot on the shelf.

ALWAYS REMEMBER: The first hurdle with launching any product is making sure you actually get picked up by distributors during their calls. Understanding the SKU mix currently in market is absolutely essential to getting there.

2021 SKU PREDICTION

Again, this is subject to many variables. The discretion of distributors and their willingness to pick up additional products is going to be pivotal. Hopefully LPs come with unique offerings that make it a no brainer to be picked up. Come on strain scientists. DO YOUR THING!

| PREDICTION OF SKUS IN THE MARKET AS OF DECEMBER 2021 | ||||||||

| Flower | Edibles | Vape | Topicals | |||||

| JAN 1 | DEC 31 | JAN 1 | DEC 31 | JAN 1 | DEC 31 | JAN 1 | DEC 31 | |

| British Columbia | 160 | 355 | 93 | 295 | 116 | 195 | 8 | 40 |

| Alberta | 412 | 600 | 118 | 320 | 237 | 3 | 10 | 48 |

| Ontario | 287 | 500 | 98 | 330 | 210 | 300 | 15 | 56 |

Alberta has a large lead in terms of SKU count in flower over the other markets. I expect to see a rise here as new genetics keep pouring into the industry and package sizes become more varied than the 3.5g. However, Ontario and British Columbia will see a higher percentage growth as they have taken on fewer SKUs to date, but the category will continue to fill.

This is the year of edibles. There is going to be a large swing in edibles brands coming to market. With a better understanding of packaging, the regulations, testing and the process, more edibles products are going to hit the market this year than any other category. There is more room for edibles products because distributors do not have to pay as much per unit to carry additional stock as other categories like vape and topicals.

Vape is likely going to cool off. There have been huge swings in this market dynamic from a wholesale and retail price standpoint. What was once seen as one of the most important categories for market entrants is going to lose its lustre when they realize margins are being squeeze beyond belief. However, downward price pressure is going to breed innovation. To regain higher margins, LPs are going to be pivoting to introduce more sophisticated product line ups.

The topicals category is going to experience moderate growth this year. Excited for it to see some love and attention, 2021 isn’t going to be that huge in terms of new market entrants running to market with products. 2022 is the year of the topical.

Onwards to Brand Leveraging

Cannabis Brand Leveraging: Cross Country Expansion

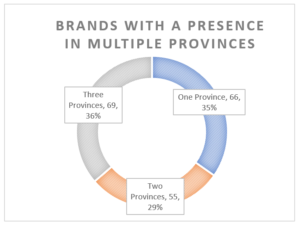

When investing in launching a brand, it is important to get the most out of it. Sure, grand plans of dominating the market nation-wide is at the top of the goals list for many LPs and it begs the question. How many brands are really pushing across the country and hitting all three of these major markets right now?

Reconfiguring the data pulled from each online store, one can identify which brands show up in each province. In total, there are 190 unique brands in the three markets. To be clear, when instances where a company has gone the “reserve” route such as “Qwest” and “Qwest Reserve”, they have been classified these as two unique brands. Fine.

Data sources: bccannabisstore.ca, ocs.ca, albertacannabis.org on Jan 1, 2021.

As shown, of the 190 total brands, it is nearly an even split evenly among each of the groupings. 69 brands are currently in three markets, 55 brands are actively in two markets, and a surprisingly large, 66 brands, are only actively selling in one of the three provinces. The number and percentage of unique brands is going to be interesting to watch over the coming months as big players only coming online now with additional brands are pushing them across multiple territories. Watching the roll out of Valen’s new-ish line of vape carts, Verse was a good example. It began in select markets and likely waited for initial sales data to roll in. Then with the positive reception, their true expansion began. It sure felt calculated and it felt well considered.

2021 Prediction for Cross Province Expansion

It is expected that the presence of single market LPs will actually increase this year as a result of the increase in micro-license issuances as smaller LPs. Micro’s are not capable of producing large enough quantities to satisfy the purchasing demands from more than one of these larger markets. As of writing, there are 140 micro licenses granted. This will continue to push the total number of single market players higher and higher. 2021 will begin to feel more like true craft.

Cannabis Brand Leveraging: Cross Category Brands

All brands are built differently. They should be formed and developed with the target market in mind. Always. Not all brands make sense to be expanded across multiple product lines either. No one needs or wants Ford branded hot sauce… right?

To properly launch a brand, it costs from tens to hundreds of thousands of dollars to achieve the proper design, messaging and brand penetration to achieve success. Given the costs associated, it would be expected that brands would conceive of their brand and its possibilities ahead of entering the market to reduce back-end spending to push multiple brands simultaneously.

With proper consideration and a little capital upfront one can drastically reduce the overall amount of money spent to reach the target market. A proper name or logo can really lighten the amount of messaging needed to achieve the desired outcome.

Given the need to segment the market based on target demographics, it is not always appropriate to use the same branding across multiple product categories. It needs to make sense. It needs to communicate the right message in each category. It makes coming up with a brand more difficult if this is your intention, but it certainly isn’t impossible. Brandolier has built plenty of brands that can work cross-category while also displaying enough depth to resonate with targets

Considering these added costs to properly develop and launch a brand and the cash outlay sensitivity that has struck fear across the cannabis industry, there remains a lack of proper brand leveraging. With each new brand, you need to start from near zero with your consumer base instead of doubling down on accrued brand equity.

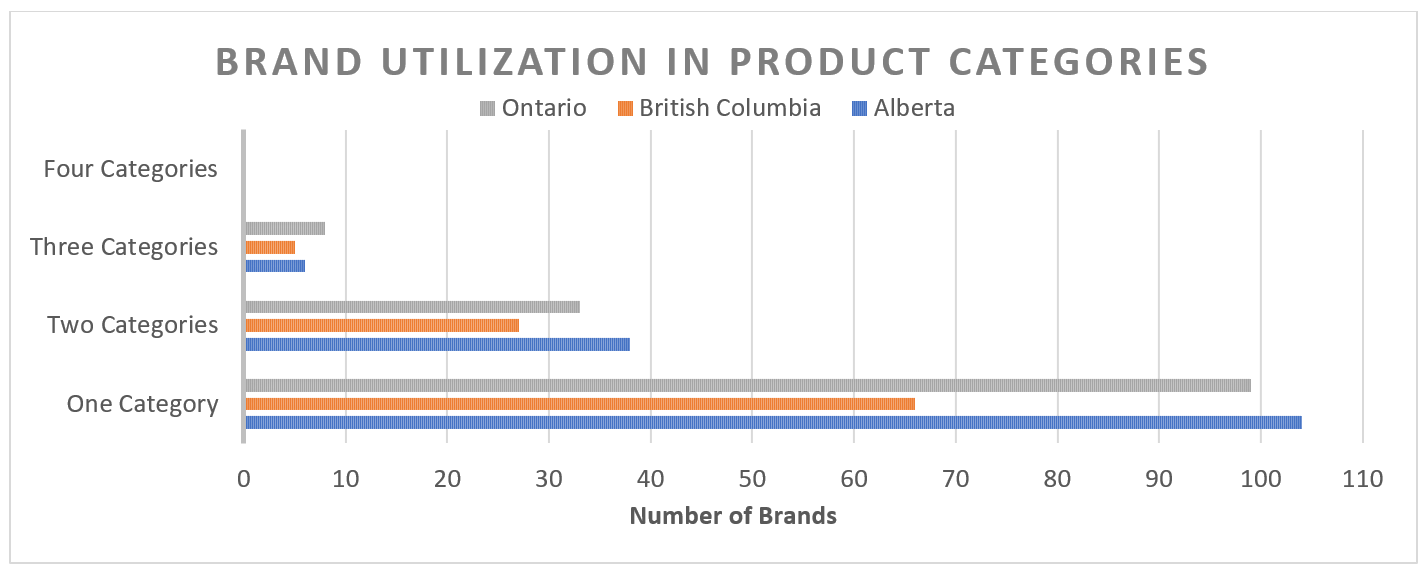

Using the four main categories previously mentioned, flower, edibles, vape and topicals, it can be seen how often the same brand is used across more than one category.

Data sources: bccannabisstore.ca, ocs.ca, albertacannabis.org on Jan 1, 2021.

Roughly 70% of brands are competing in just one of the four categories. One might think that this is solely due to the higher brand count competing in flower alone. While this does explain some of what is happening, that is not the whole story. There are plenty of beverage only, edible only, topical only, and vape only brands not participating in the flower space.

2021 Prediction for Cross-Category Brands

Drumroll please. Product branding is becoming more nuanced in the cannabis industry. This has been a recent development, but a bit more sophistication has been shown which is appreciated. One category brands are here to stay for 2021 and the percentage of total brands operating in multiple categories is likely to stay around the same. This is due to the same reasons that brands aren’t stretching into multiple provinces. 2021 will see more micro LPs and newer LPs entering the fray. These competitors will not have either the capacity or experience to stretch too big too quickly without straining their resources.

Although the percentage might not change, 2021 will see an overall increase in multiple category brands. Larger LPs with already established brands will begin migrating them into new spaces to begin reaping the rewards of brand equity.

OVERALL

2021 is going to be a big year for the Canadian cannabis industry. With the first full year of cannabis 2.0 products being available, the follow up year is going to help define what this industry has to offer. Product mixes will change, brands will be better developed, consumer recognition will increase and last but definitely not least, there is going to be GROWTH. GROWTH. GROWTH.

…no pun intended.